Moody's, S&P give blessing to DSSI participation; SADC summit brings Angola and DRC to the virtual table

Welcome to the Angola Economic and Political Risk Briefing for 11 August 2020

Welcome to the Angola Economic and Political Risk Briefing, Issue 20

by Zitamar News, Moxico Risk Consulting LLP, and Mark Bohlund

Good morning. Ratings agencies Moody’s and Standard and Poor’s have both acknowledged potential benefits to Angola and other sovereigns from participating in the G20 Debt Service Suspension Initiative (DSSI) — and that the initiative need not make private sector creditors nervous. However, any upside to Angola’s creditworthiness from a debt service moratorium is going to be constrained by its declining oil revenue, and any moratorium is likely to add to its medium-term debt repayment obligations, although debt-for-equity swaps with China Development Bank are a possibility.

The Southern Africa Development Community (SADC)’s 40th Ordinary Summit is getting underway this week, (virtually) hosted by Mozambique, whose troubled province of Cabo Delgado will give member countries food for thought — and possibly friction.

Angola’s hospitality sector has won some relief from covid-19 restrictions, although financial support is still under discussion. And South African retailer Shoprite has announced a downsizing of its operations in Angola, while stopping short of a total withdrawal as it has done from the Nigerian market.

In this issue

Economy:

S&P suggests some upside to Angola from DSSI (Standard & Poor's)

Moody’s decides against downgrading DSSI-participating sovereigns (Moody’s)

Politics:

SADC 40th Ordinary Summit of Heads of State gets underway (Jornal de Angola)

Restaurants and commercial spaces get extended opening hours as home quarantine rules tighten (Valor Econômico)

Shoprite closes two supermarkets in Luanda in wider African downsizing (Valor Econômico)

S&P suggests some upside to Angola from DSSI (Standard & Poor's)

Standard and Poor’s affirmed their CCC+ rating of Angola on 7 August, stating that low oil prices, rapid currency depreciation, and the economic impact of covid-19 are accentuating external and fiscal deficits and increasing financing pressure. While S&P maintained the stable outlook on its CCC+ rating, which signals a substantial risk of default, it did say ongoing debt reprofiling negotiations with official lenders could provide some immediate breathing space, albeit adding to repayments in 2023 and onwards.

The rating update correctly highlights how the combined effect of low oil prices, cuts to oil production and covid-19 is intensifying pressure on Angola's debt-servicing ability, external buffers and debt burden — though we view currency depreciation as a net positive for debt servicing, albeit with substantial socio-economic costs. More interesting are S&P’s views on the ongoing negotiations for a reprofiling of Angola’s external debt, most importantly with China. Their comments on the potential debt reprofiling highlight the short-term gain of an immediate liquidity relief, counterbalanced by a heavier debt repayment profile once the moratorium has ended. This will limit the upside to Angola’s current rating, which is already constrained by declining oil revenue. Nonetheless, we still see potential for an upgrade in S&P’s rating to B- if Angola can secure a multi-year debt moratorium from China with an extended repayment profile as well as financial support from the IMF.

The treatment of loans from China Development Bank is probably a key factor holding up the debt restructuring negotiations with China which began in early June. Comments from World Bank President David Malpass have highlighted China’s opposition to including CDB loans in the DSSI, likely on the grounds that they were extended on commercial terms and should not be viewed as official bilateral debt. As we have noted previously (see Angola Economic Briefing - 19 June), Angola’s negotiations with China for debt relief raise the likelihood for debt-equity conversion operations including offshore oil fields as well as a stake in Sonangol, which was recapitalised with the help of a $10bn loan from China Development Bank in 2016 and is due to be partially privatised through the government’s ProPriv programme. We expect such debt-for-equity swaps to be viewed positively by the IMF, the World Bank and rating agencies, but to be criticised by the current US administration.

Moody’s decides against downgrading DSSI-participating sovereigns (Moody’s)

Moody's concluded its review for downgrades for the five sovereigns that it covers that will take advantage of the G20 Debt Service Suspension Initiative (DSSI): Cameroon, Côte D’Ivoire, Ethiopia, Pakistan and Senegal. The ratings agency said that while it does believe that the DSSI poses risks to private creditors, its decision to conclude the review and confirm the ratings reflects its assessment that those risks are adequately reflected in current ratings, and that the probability of private sector involvement in the initiative appears to have diminished.

It has become increasingly clear that any private sector participation in the DSSI would be voluntary on the part of creditors, so there is no need for countries to suffer downgrades if they benefit from the scheme. Angola’s B3 rating at Moody’s is on review for downgrade due to the effects of the coronavirus pandemic, the shock from the sharp drop in oil prices, and an acute tightening in global financing conditions on Angola's already weak public finances and external position, and elevated government gross borrowing requirements. A completion of the debt reprofiling negotiations with China and approval of the latest IMF review should prompt Moody’s to end the downgrade review, but any upside will be limited by Angola’s challenging public and external debt metrics.

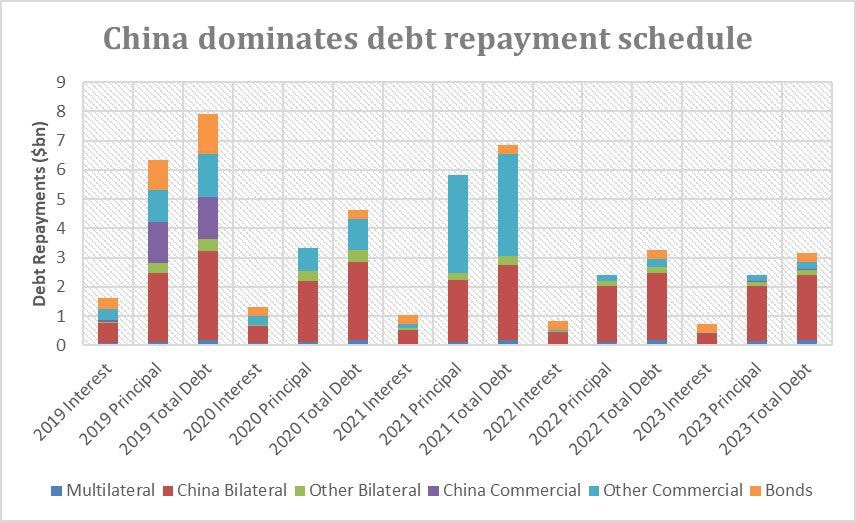

Chart of the Day

SADC 40th Ordinary Summit of Heads of State gets underway (Jornal de Angola)

On 10 August the SADC Standing Committee of Senior Officials began a teleconference to prepare the documents to be discussed at the 40th Ordinary Summit of Heads of State and Government in the region. Mozambique is hosting the virtual meetings, as it takes over the rotating chair of the bloc. Angola’s delegation is headed by President Lourenço and Minister of Foreign Affairs Téte António. The summit will analyze the socio-economic impact of covid-19 as it relates to SADC members, as well as formulating the post-2020 agenda.

The 40th Ordinary Summit is operating with a reduced agenda, owing to the limitations posed by the covid-19 pandemic. The management of this event is handled by a Troika, which comprises the current SADC chairperson (President Magufuli, Tanzania), the incoming chairperson (President Nyusi, Mozambique) and the previous chairperson (President Geingob, Namibia). The Troika responsible for the SADC Organ on Politics, Defence and Security Cooperation comprises President Mnangagwa (Zimbabwe) as the incumbent chairperson, President Lungu (Zambia) as his predecessor and President Masisi (Botswana) as the incoming chairperson. The summit’s security organs will likely discuss two issues relevant to Angola: the spillover of the Cabinda insurgency into neighbouring countries, and potential SADC involvement in combating the Cabo Delgado insurgency in Mozambique.

The Angolan Armed Forces’ repeated territorial incursions into the DRC over the past two months led DRC Interior Minister Gilbert Kankonde to threaten to report the issue to relevant sub-regional organisations such as the SADC (see Angola Economic Briefing - 22 June 2020). Disputes over these incursions at the SADC level would likely contribute to further political tensions between Angola and the DRC, which would impact on a number of bilateral issues, including President Lourenço’s anti-corruption asset recovery initiative and the ongoing maritime boundary dispute (see Angola Economic Briefing - Tuesday 30 June 2020).

It seems highly unlikely that the SADC will organise a counterinsurgency military intervention in Cabo Delgado, despite the Troika, led by Zimbabwe’s Mnangagwa, encouraging SADC members to help out. Rumours that Zimbabwean and even Angolan troops are already on the ground are very likely false. Likewise, a report on 29 July from Africa Intelligence, claiming that the South African military “stands by to go into Cabo Delgado” was judged inaccurate by the ‘Cabo Ligado’ conflict observatory project, a joint venture between ACLED and Zitamar News. The Angolan government would be highly wary of committing troops to Cabo Delgado, and equally wary of allowing regional rivals South Africa to do so on a bilateral basis. The SADC Organ on Politics, Defence and Security Cooperation is therefore unlikely to offer more than expressions of solidarity and possibly financial support for Mozambique’s efforts in Cabo Delgado at the end of this week.

Restaurants and commercial spaces get extended opening hours as home quarantine rules tighten (Valor Econômico)

As of Monday 10 August, restaurants can operate at 50% capacity from 6am to 9pm, with takeaway services offered until 10pm. Commercial establishments can now operate from 7am to 7pm, with capacity limited to 50% in Luanda Province, and 75% in other provinces. Fines for violating the home quarantine regulations have also been increased, and individuals are not allowed to leave home quarantine without a discharge certificate issued by Angola’s health authorities.

The extended opening hours will come as a significant relief to Angola’s restaurateurs and other business owners who have suffered a severely restricted operating environment since 27 March. The sector, made up of around 4,000 restaurants in Angola, has shown surprising resilience throughout this crisis, adapting as necessary to offer delivery food instead of in-person dining. However, the Association of Angolan Hotels and Resorts noted that covid-19 was putting over 150,000 jobs at risk in the wider hospitality industry, and despite discussions ongoing since April, no emergency fund has been put in place to support this industry, increasing contract non-payment risks for hospitality industry suppliers.

Shoprite closes two supermarkets in Luanda in wider African downsizing (Valor Econômico)

On 31 July Shoprite closed two of their minimarkets in Luanda, in Zango and Mulemba. Over the past three years, Shoprite has also closed locations in Bela Vista, Lobito, Matala, Huila, and Porto Amboim. On 3 August Shoprite announced a complete withdrawal from the Nigerian market. The supermarket noted that their most recent closures in Angola were not an indication of a “lack of confidence” in the Angolan market, but that they had suffered losses of over 8% in Angola, and that the model of minimarkets (such as in Zango and Mulemba) was not viable.

These latest closures indicate further trouble at the South African supermarket chain, that recently suffered a suspicious fire in their Cacuaco branch and is unable to open their newly built stores in Cabinda or Luena until the sanitary cordon around Luanda Province is lifted. Shoprite’s own financial results presentation for H2 2019 shows that Angola’s introduction of 14% VAT in October 2019, combined with the drastic devaluation of the Kwanza led to -27.5% sales growth in ZAR terms, a situation which has only been exacerbated by the covid-19 restrictions put in place after 27 March. Multiple Angolan news outlets are quoting South African market analysts saying that Shoprite may discontinue operations in Angola in order to strengthen the group's business in South Africa. With over 20 stores in Angola, and considering the profitability of the Angolan market pre-2018, in the six month outlook Shoprite is more likely to reduce their exposure to the market by further downsizing their Angolan operations, closing more of their smaller minimarkets or supermarkets in the interior that are more of a logistical challenge to keep stocked. This will put many of Shoprite’s 4,000 Angolan workers at risk of redundancy, further increasing protest risks.